As a means of drawing income in retirement, annuities have made a significant comeback, and for good reasons. Once considered the “forgotten” retirement product, they are now reclaiming their place at the heart of financial planning.

From “Pension Freedoms” to a Resurgence

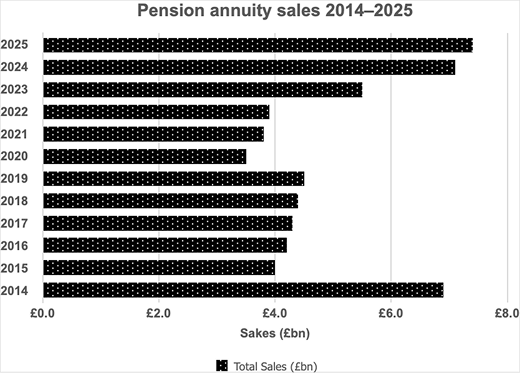

In 2014, then-Chancellor George Osborne transformed the retirement landscape by ending the effective requirement to convert pension plans into annuities. These “pension freedoms” sent shockwaves through the industry, and annuity sales plummeted from nearly £7 billion in 2015 to just £4 billion a year later.

However, the tide has turned. Driven by higher interest rates and a shift in investor sentiment, the latest 2025 figures from the Association of British Insurers (ABI) show that £7.4 billion was invested in annuities last year—surpassing the levels seen before the 2014 reforms. While inflation means this is still lower in “real” terms than a decade ago, the momentum is undeniable.

The Rise of the “High-Value” Annuity

The ABI data reveals that it isn’t just volume that is increasing, but the size of the commitments.

-

Large Pot Growth: Sales of annuities with purchase prices over £250,000 rose by 31%, while those above £500,000 surged by 54%.

-

Later-Life Security: There was an 8% rise in sales to individuals aged 70 and older, as retirees look to lock in certainty during their later years.

-

Inflation Protection: Escalating annuities—which increase payments annually to protect purchasing power—now account for one in five of all sales.

Navigating the 2027 Inheritance Tax “Cliff Edge”

The surge in high-value sales is likely a strategic response to upcoming legislation. From 6 April 2027, unused pension pots will be brought within the scope of Inheritance Tax (IHT).

For many, this creates a potential “double tax” trap. If a pension holder dies after age 75, the combined impact of IHT (40%) and the beneficiary’s income tax (up to 45%) could lead to an effective tax rate of 64% or higher. By converting a pension into a lifetime annuity, the “unused pot” is removed from the IHT calculation, providing a guaranteed, tax-efficient income stream for life. At current rates, a 65-year-old could see an inflation-linked income starting at over 5.25% annually.

Is an Annuity Right for Your Retirement?

With the 2027 tax changes looming and interest rates offering the best value in over a decade, there has never been a more important time to review your retirement strategy. Whether you are looking for the security of a guaranteed income or seeking to mitigate a future IHT burden, professional advice is essential.

At Chartwell Wealth Management, we can help you weigh the benefits of annuities against flexible drawdown to find the right balance for your legacy. Contact us today to arrange a comprehensive review of your pension and estate plans.

Important Information:

The value of your investment and any income from it can go down as well as up and you may not get back the full amount you invested. Tax treatment varies according to individual circumstances and is subject to change. The Financial Conduct Authority does not regulate tax advice.