“How long am I going to live?” is a question that carries more weight the older we get. While many turn to the Office for National Statistics (ONS) life expectancy calculator for a quick answer, the raw numbers often mask a more complex reality.

For a one-year-old boy, the average life expectancy is 87 years—four years less than his twin sister. At age 65, those averages shift to 85 for men and 88 for women. However, these figures are merely starting points.

The Problem with Averages

Averages can be misleading because they don’t account for individual variance or lifestyle. For instance, the ONS calculates that a 65-year-old man has a 1-in-4 chance of reaching 92, while a woman of the same age has a 25% chance of reaching 95.

Furthermore, these national figures bundle together vastly different lifestyles and demographics:

-

Lifestyle Factors: The data includes both non-smokers and the 12% of the UK adult population who still smoke.

-

Regional Disparity: ONS research highlights a staggering ten-year difference in male life expectancy at birth between areas like Blackpool and the London Borough of Kensington and Chelsea.

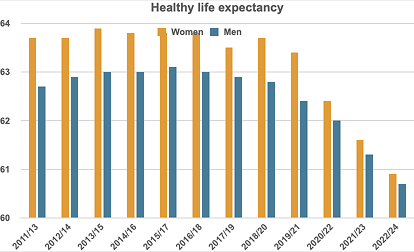

The Rising Importance of “Healthy Life Expectancy”

While we often focus on the total number of years, a more critical metric for financial planning is healthy life expectancy. This measures the average time an individual can expect to live in “very good” or “good” general health.

Latest ONS research published in February 2026 (using 2022–24 data) reveals a sobering trend at birth:

-

Men can expect a healthy life expectancy of just 60.7 years.

-

Women can expect a healthy life expectancy of 60.9 years.

Crucially, these figures have dropped by 1.8 years for men and 2.5 years for women compared to the previous 2019–21 period. This suggests that while medical science may be keeping us alive longer, we are spending a greater portion of our later years in declining health.

Bridging the Financial Gap

The widening gap between total life expectancy and healthy life expectancy has profound consequences for retirement. If your “healthy” years end in your early 60s, but you live until your late 80s, you may face over two decades of increased costs related to care, mobility, and health-related wellbeing.

Building a dedicated reserve fund to manage the costs of failing health is no longer a luxury—it is a cornerstone of a resilient long-term financial plan.

Plan for a Healthier Future with Chartwell

A truly robust retirement strategy accounts for both the years you want to enjoy and the years where you may need extra support. At Chartwell Wealth Management, we help you look beyond the averages to create a personalised plan that protects your lifestyle and your legacy, no matter what the future holds.

To ensure your financial plan is prepared for the long term, contact us today for a comprehensive review of your retirement provision.

Important Information: The value of your investment and any income from it can go down as well as up and you may not get back the full amount you invested. Tax treatment varies according to individual circumstances and is subject to change. The Financial Conduct Authority does not regulate tax advice.